Purchasing Real Estate with Physical Precious Metals from a Bonded Warehouse: What’s Really Behind It

April 21, 2026

Publisher: Spargold GmbH | spar.gold

Date: April 2026

Reading time: approx. 8 minutes

“Silver is stored in a bonded warehouse — and it can even be used to pay for real estate.”

This sentence is increasingly heard in tangible asset communities. What is behind it? And where does legal structuring and professional advice end — and dangerous half-knowledge begin?

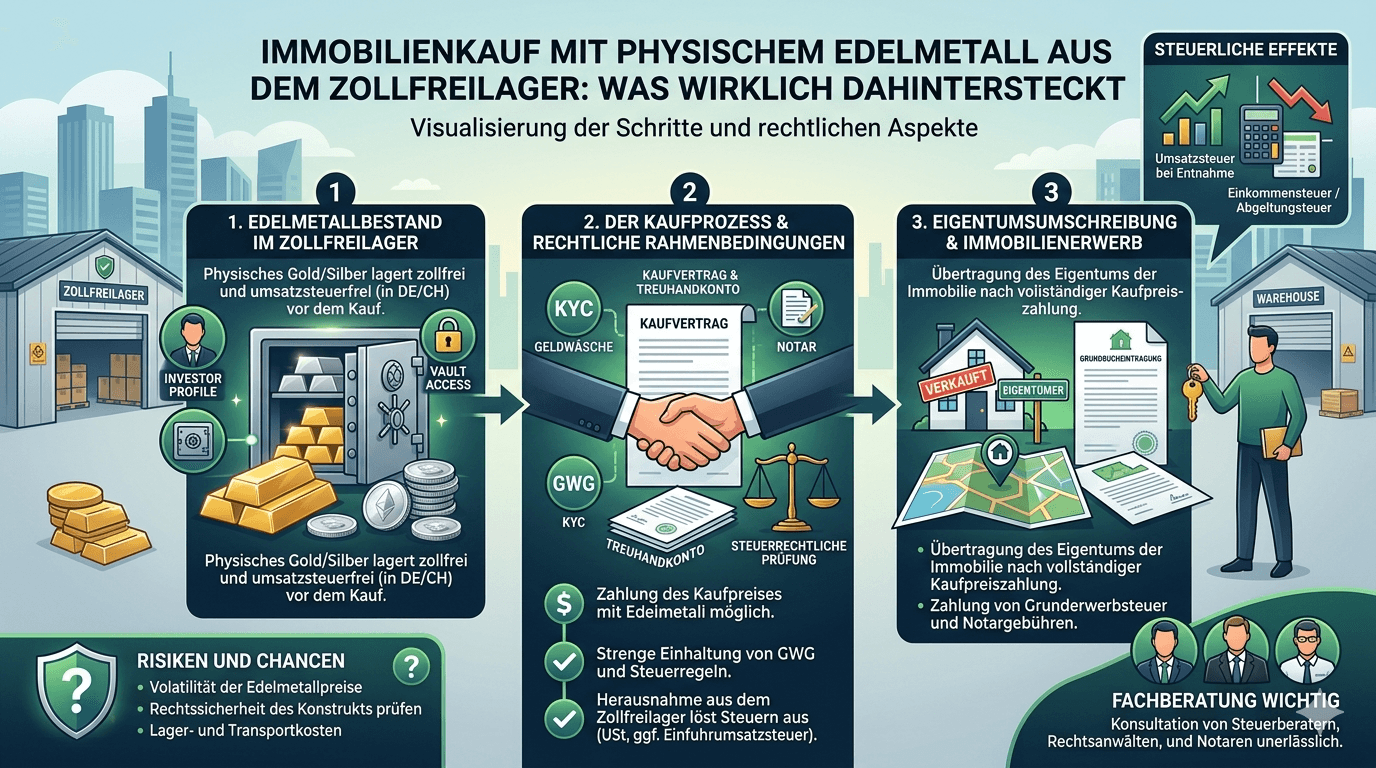

A bonded warehouse (Zollfreilager) is a transit area monitored under customs law. Goods stored there are formally not considered imported into an economic territory. As long as silver, platinum, or palladium remains in the warehouse, no value-added tax (VAT) is incurred — neither at the storage location nor in Germany.

This is not a trick or a gray area: Bonded warehouses have existed for decades, are officially approved, and comply with international trade law. For German private investors who want to hold white metals long-term, this is a completely legal instrument for asset optimization.

Well-known locations include Switzerland (Zurich, Geneva), Singapore, and Liechtenstein. Common to all: They are located outside the EU customs territory and are subject exclusively to the respective national law — not the German UStG.

What has changed: German bonded warehouses have been practically devalued by the new regulation on § 4 No. 4b UStG (BMF letter dated April 9, 2026). Warehouses outside the EU are not affected by this change.

A model is circulating in the tangible asset community that looks like this in its basic structure:

A real estate buyer owns precious metal holdings in a bonded warehouse outside the EU — for example, in Switzerland or Singapore. Instead of paying the purchase price via bank transfer, he transfers ownership of a corresponding holding directly within the warehouse to the seller. No metal moves, no customs duties become due, and no local VAT is incurred.

The idea sounds elegant. It is also not fundamentally illegal. However, it is significantly more demanding in terms of requirements than it appears at first glance.

Anyone using precious metal as a purchase price payment is disposing of it for tax purposes. It is a private disposal transaction according to § 23 Para. 1 No. 2 EStG — even if no money flows, but an exchange takes place.

Consequence: The holding period of the precious metal must be at least 12 months at the time of the transfer of ownership. Otherwise, the entire increase in value must be taxed at the personal income tax rate. For larger positions, this can quickly amount to six-figure sums. Only after the one-year period has expired is the capital gain tax-free for private individuals.

Documentation Obligation: Purchase receipts with date, quantity, and cost price must be kept. Anyone who cannot produce these will have a serious problem in the event of an audit.

Real estate transfer tax (depending on the federal state, 3.5 to 6.5% of the purchase price) is due regardless of the chosen payment method. The assessment basis is the market value of the property — not the nominal equivalent value of the precious metal used.

The notary is obliged to report the actual economic equivalent value. Attempts to reduce the GrESt base through valuation manipulation are relevant under criminal tax law.

Real estate purchases in Germany strictly require notarial certification (§ 311b BGB). The purchase price must be described precisely and completely in the contract.

A purchase price payment through the transfer of ownership of precious metal in a bonded warehouse outside the EU is representable by a notary — but requires very precise contract drafting: - Exact description of the transferred holding (metal, quantity, storage location, depot designation) - Valuation basis (daily rate of which reference? On which reporting date?) - Mechanism of ownership transfer in the warehouse (rebooking confirmation from the warehouse operator) - Maturity construction: When is the purchase price considered paid?

Many notaries will reject this construct for precautionary reasons or insist on very specialized legal advice.

Notaries are obliged to identify and assess risk according to § 10 GwG. A real estate payment in the form of precious metal holdings abroad is by definition an unusual transaction and triggers enhanced due diligence obligations.

In case of doubt, there is a reporting obligation to the FIU (Financial Intelligence Unit). This also affects the buyer indirectly: He must be able to document the complete origin and tax treatment of his holdings without gaps.

The seller who receives precious metal instead of money acquires foreign assets. These must be: - Declared in the German income tax return - Subject to their own one-year period upon later sale (from his date of acquisition) - Treated as business income if there is a commercial background

Many private sellers will simply reject this model — because they need liquidity, not precious metal holdings in Zurich or Singapore.

Plain language must be used here — especially by us at Spargold.

The model exists. It circulates in tangible asset communities and is discreetly promoted by individual providers — occasionally with the subtext that transparency towards the tax office is optional. This is exactly what is dangerous.

What remains upon closer inspection:

The tax advantages of this model are real — but only if all requirements are met. In particular, the 12-month period is non-negotiable. Anyone who uses holdings built up less than a year ago for a real estate payment realizes a taxable profit. Ignorance is no excuse.

The idea of operating permanently below the radar of the tax authorities through clever construction is an illusion. Automatic information exchange programs (OECD-CRS, FATCA) are increasingly being extended to tangible asset depots and bonded warehouses outside the EU — both in Switzerland and Singapore. The international consensus to fully record assets abroad remains politically unbroken.

The actual problem does not lie in the instrument itself. It lies in the way it is communicated: often as an uncomplicated tax-saving path, rarely with a full presentation of all obligations and risks. Anyone who leads customers into such constructs without ensuring the complete tax advisory chain is acting negligently — at best.

At Spargold, our standard is different: We are building a platform where physical precious metal works transparently, compliantly, and permanently as an asset component. This includes naming uncomfortable truths — even if they make our own subject matter more complicated.

Purchasing real estate with precious metal from a bonded warehouse outside the EU is not a product of fantasy. Under the right conditions, it is legal and can be tax-efficient. The requirements are:

✓ Holding period of the precious metal > 12 months (§ 23 EStG)

✓ Full documentation of purchase, holding period, cost price

✓ Notarial certification with precise purchase price description

✓ Real estate transfer tax based on market value

✓ GwG-compliant documentation of origin

✓ Tax advice for both parties

✓ Acceptance by the seller — and his bank

If even one of these components is missing, the construct is either practically impossible to implement or risky under tax law. There are no shortcuts.

Transparency is not the lesser of two evils — it is the only way.

Anyone wishing to use this model needs an experienced tax advisor, a specialized notary, and clean, complete documentation. Anyone who shies away from this should leave it be.

Spargold GmbH is a platform for physical gold micro-savings based in Jever. We stand for transparent, compliant tangible asset investments — without shortcuts. This article serves for general information purposes and does not replace individual tax or legal advice. Further information at spar.gold

Further reading: - BMF letter dated April 9, 2026, on § 4 No. 4b UStG - § 23 Para. 1 No. 2 EStG (Private disposal transactions) - § 311b BGB (Notarial certification requirement) - § 10 GwG (Due diligence obligations for real estate transactions)

Stay farsighted

Yours, Helge Peter Ippensen