CME Record Volume 2025: Why Precious Metals are Setting the Pace and Volatility is Becoming the New Normal

February 12, 2026

The Chicago Mercantile Exchange (CME) reports a record year in commodity trading for 2025. What is striking is less "commodities" as a collective term, but rather the focus: the metals business grew particularly strongly, and within metals, it was primarily precious metals that made the difference. Exactly where private and institutional investors have been seeking protection against loss of purchasing power, geopolitical risks, and currency uncertainty for years, activity increased most significantly.

The CME data, which is highlighted in the Handelsblatt, clearly shows the pattern: metals increased significantly compared to the previous year, precious metals even more so. At the same time, demand for options grew – instruments with which market participants specifically manage price fluctuations.

A common misconception is: when gold "runs," things get calmer because many view it as a safe haven. The reality in this cycle is different. The more market participants trade in a shorter period, the stronger movements can become – both to the upside and the downside. This is exactly what the recent dynamics describe: hedging demand, increased retail access, and a very rapid response to news situations lead to a market where hedging itself can become the driver of the movement.

An example of this is margin adjustments: At the beginning of February, the CME once again raised the margin requirements for gold and silver futures, following several adjustments in quick succession. For COMEX gold futures, requirements for certain account profiles rose from 8% to 9%, and for silver from 15% to 18% – a clear indication that the exchange is actively managing the risk arising from volatility.

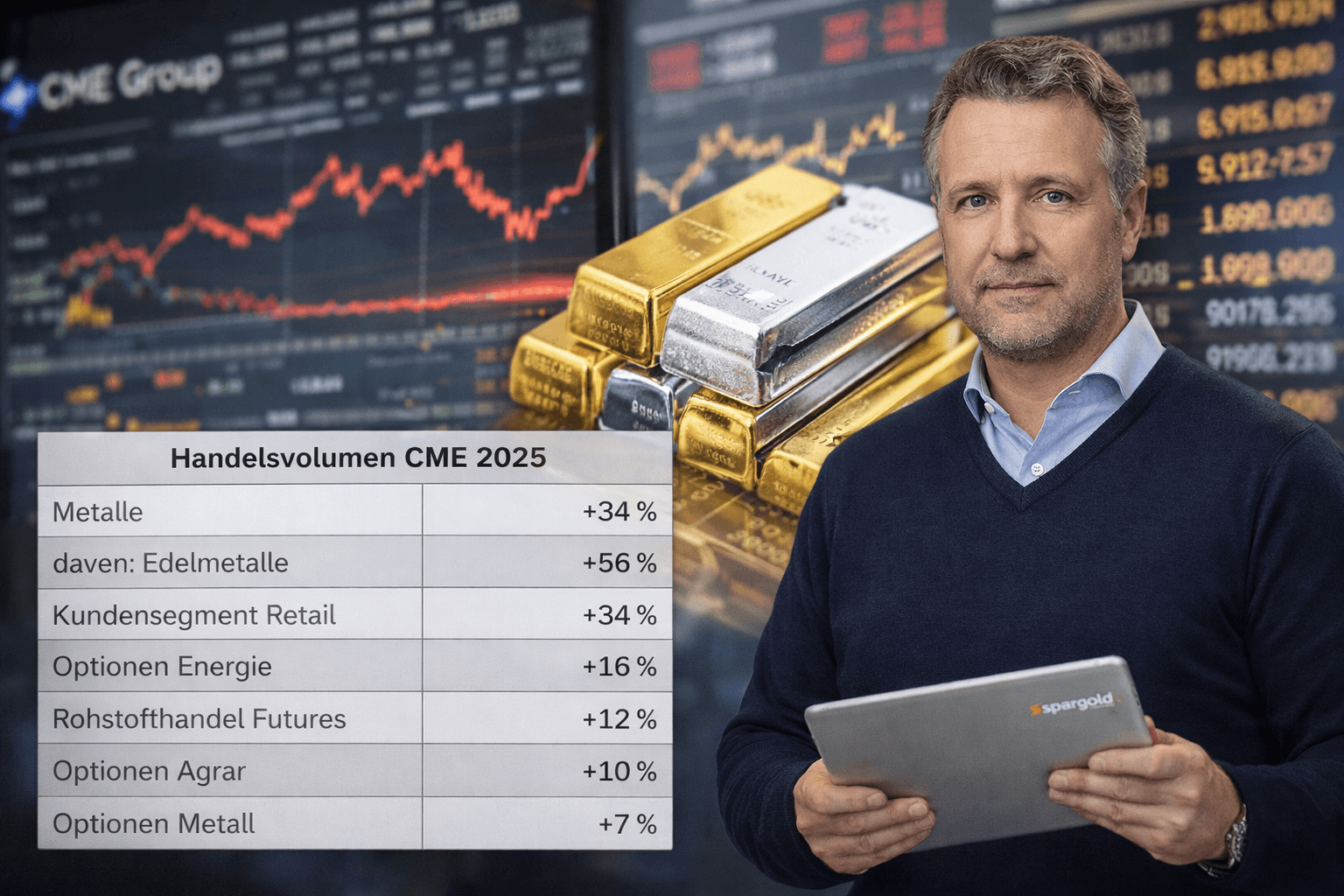

The changes summarized in the Handelsblatt show how broad the surge was – and where it was strongest.

| Segment (CME, Change 2025 vs. Previous Year) | Change |

|---|---|

| Metals | +34% |

| of which: Precious Metals | +56% |

| Retail Customer Segment | +34% |

| Energy Options | +16% |

| Commodity Trading Futures | +12% |

| Agricultural Options | +10% |

| Metal Options | +7% |

This structure is remarkable: precious metals are growing faster than the metal complex as a whole. And retail is also growing significantly, which typically changes market mechanics because positioning, time horizons, and reaction speeds become more heterogeneous.

Volatility is not just "unrest," but the measurable expression of uncertainty and positioning pressure. The Handelsblatt charts show a 90-day volatility that is significantly higher for silver than for gold – and occasionally shows extreme swings. This fits a market where silver is simultaneously an investment narrative and an industrial metal, thus reacting more strongly to economic and risk signals.

| Volatility (Example from the 90-Day View) | Level |

|---|---|

| Gold (current value in the representation) | 33.5% |

| Silver (current value in the representation) | 87.7% |

| Copper (current value in the representation) | 33.9% |

| 5-Year Average Gold | 15.2% |

| 5-Year Average Silver | 28.3% |

| 5-Year Average Copper | 26.7% |

The core message is not the exact number on a single day, but the direction: volatility is significantly above long-term averages – especially for silver.

Parallel to the record activity, a second trend is emerging: the CME is introducing contracts that facilitate access. For example, a new record in metal futures and options was reported at the end of January, and in the context of strong retail demand, the introduction of a 100-ounce silver future was also announced (starting in early February, subject to regulatory review).

The options side is also growing visibly: a CME update on metal options describes high average daily activity (ADV) for gold options at the beginning of 2026 and refers to a strong previous quarter in 2025. When more market participants use options, hedging flows typically also increase, which can amplify movements during hectic phases.

In an environment where record volumes and volatile price fluctuations occur simultaneously, a distinction becomes more important: price movement is a market signal, but not synonymous with stability. Anyone viewing gold and silver in the context of inflation, interest rates, and geopolitical uncertainty should therefore separate two levels: the long-term function as a real asset and the short-term market mechanics shaped by derivatives, margins, and positioning.

The recent margin increases in particular show: when volatility rises, the requirements for risk management also rise – and this in turn affects liquidity and tradability. For private investors, this primarily means clearly defining their own timeline and risk tolerance instead of being driven by short-term swings.

Stay farsighted

Yours, Helge Peter Ippensen